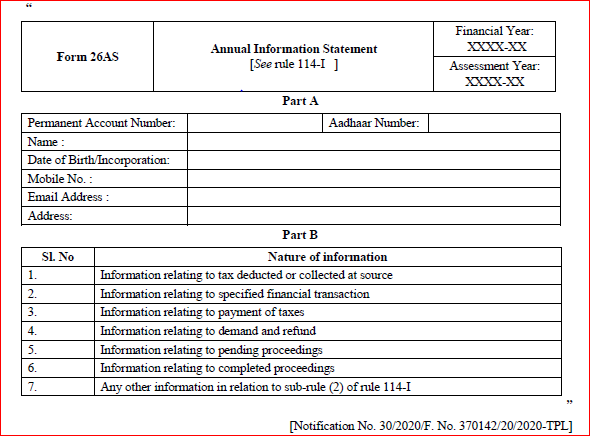

Form 26AS will now be a complete profile of the taxpayer w.e.f. 01.06.2020. CBDT vide Notification dated May 28, 2020 amended Form 26AS in Sec 285BB w.e.f. 01.06.2020.

New form 26AS will also provide information in respect of “Specified financial transactions” which include transactions of purchase/ sale of goods, property, services, works contract, investment, expenditure, taking or accepting any loan or deposits of such value as may be prescribed but not less than of Rs 50,000.

Information about income tax demand, refund, proceedings pending, and proceedings completed which may include assessment, reassessment under section 148,153A 153C, revision, appeal will also be shared in this form 26AS.

Information on this form 26AS will not be a one-time affair at year end. This will be a live 26AS, as this will be updated regularly within 3 months from the end of the month in which such information is received.

Form 26AS will now be a complete profile of the taxpayer for that particular year as against earlier form 26AS which just provided the information about taxes paid by way of TDS/TCS or self-assessing.

This form will also have mobile no, email I’d and Aadhar no. of the taxpayer.

Further an enabling provision has been notified empowering the CBDT to authorise DG Systems or any other officer to upload in this form, information received from any other officer, authority under any law. Thus any adverse action initiated or taken or found or order passed under any other law such as custom , GST , Benami Law etc. including information about Turnover , import , export etc. will also be put in this form 26AS so that not only the concerned taxpayer but also all the Income Tax authorities will know and have access to such information.

This form 26AS will also provide information received by Tax Deptt from any other country under the treaty /exchange of information about income or assets of the taxpayer located outside India.

The implication of this new form 26AS will be that banks , financial institutions or any other authority or customer , buyer etc. while carrying out due diligence of the person/ corporate concerned will now ask for form 26AS so as to be sure that there are not any major issues about such person/corporates.

This will now make difficult for any taxpayer to hide information from any bank / financial institution/ authority about any proceedings against under any law or tax demand, tax disputes etc.